Both Hands on the Wheel

How, in a single year, the United States took up the tools of state control it always said belonged to China, and why it was inevitable.

On the last day of April, 2021, a new shareholder appeared in the corporate records of Beijing ByteDance Technology, the subsidiary that holds the licenses allowing ByteDance to push video and news onto a few hundred million phones across China.

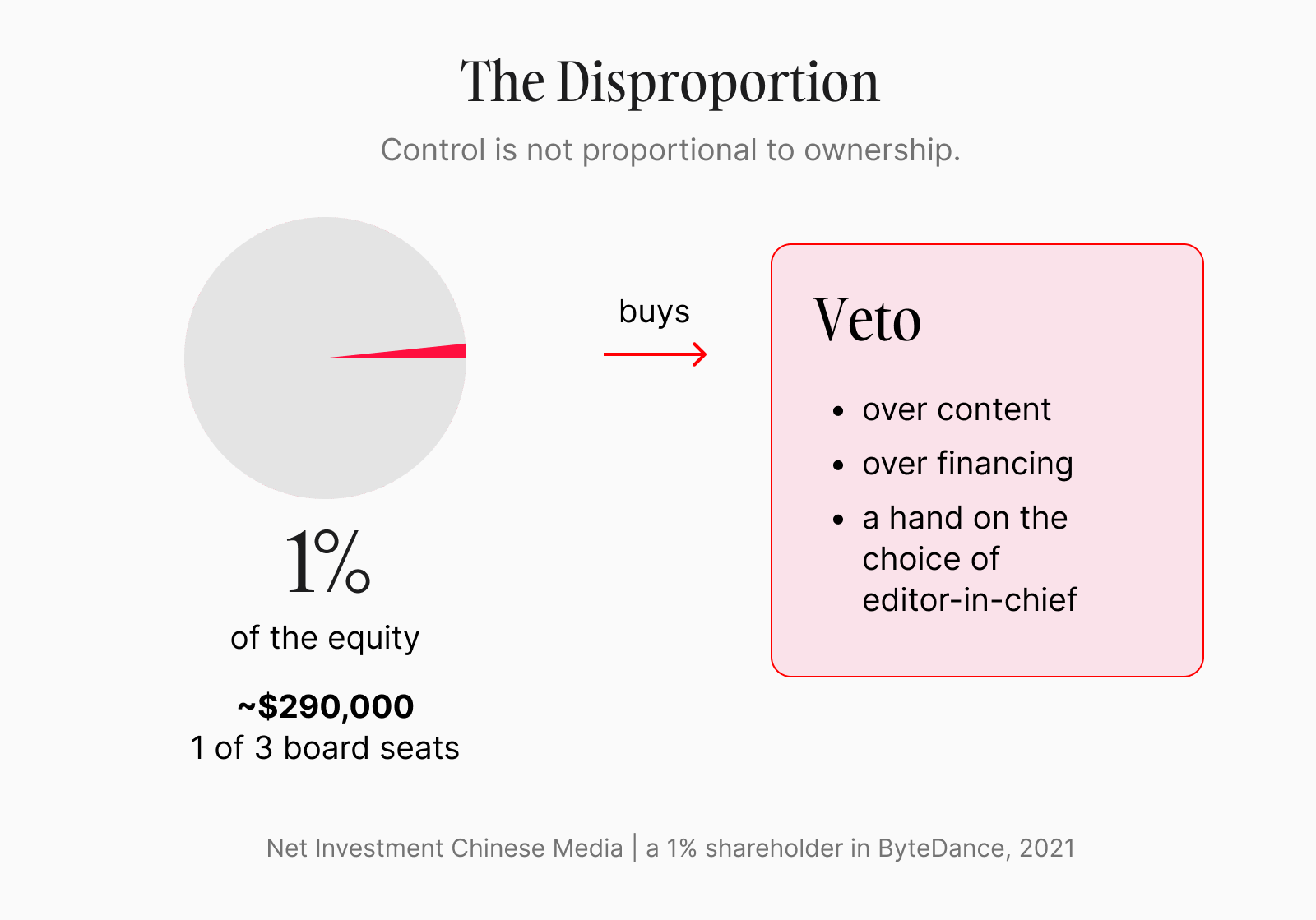

A week earlier, it had not existed. It was called WangTou Zhongwen, a name that rendered in English as something very forgettable: Net Investment Chinese Media. No one could locate its offices or name its staff. The stake it bought came to one percent, and the price, when the reporting finally pried it loose, was about 2 million yuan (roughly 290,000 dollars). The company, now part-owned, was worth a quarter of a trillion. The 2 million yuan was loose change. The one percent came with a seat (one of three on the board) plus a veto over the only two questions that decide what a company like ByteDance is: what the platform shows the people who open it, and where it gets the money to keep going. The seat went further still; scholars who later took the structure apart found it resting a hand even on the choice of the editor-in-chief.

The arrangement has a name in Chinese: 特殊管理股, the special management share. By the time it reached ByteDance it had been circulating through the country’s media companies for half a decade, always in the same plain costume. A state-backed fund takes a sliver of equity, around one percent. With it comes a director, and a veto over the short list of decisions the Party minds most. Weibo had disclosed a nearly identical setup to American securities regulators a year before. Kuaishou had one. So did corners of Alibaba and Tencent. In none of these cases did the state buy the company. It took a chair and a veto and left the rest of the shares where it found them, in private hands, on a private balance sheet, held by people who were now, in the ways that counted, no longer in charge of them.

For years, the special management share read as a foreign specimen, the kind of quiet instrument that surfaces where the Party sits inside the firm and never where it does not. People who track these things took it exactly that way. Pablo Chavez, who has run public policy for Google, Microsoft, and LinkedIn, read about the ByteDance stake and set the reflex down almost word for word: it looked, he wrote, like something Beijing would do and Washington never would.

He turned out to be wrong. Over a single year the United States reached for the same kind of control, deliberately, and in the open. It did so as a direct answer to China: industrial tools Washington had treated as foreign, even un-American, for the better part of a century, picked back up because it had concluded that a country which keeps both hands off the wheel cannot compete with one that does not. The instrument did not migrate home on its own. A government went and got it.

The story of why Beijing wanted so quiet an instrument runs through a man who was the opposite of quiet, on a stage on the Shanghai waterfront, in the autumn of 2020.

On the evening of the 24th of October, Jack Ma walked out in front of the Bund Summit, a finance conference whose audience was thick with the central bankers and regulators who run the Chinese economy. He was the most celebrated businessman in the country, a former English teacher who had built Alibaba into a colossus. In nine days he would take its payments arm, Ant Group, public in a dual listing in Shanghai and Hong Kong, an offering set to raise around 37 billion dollars and value the company north of 310 billion. It was the largest in the history of the world. The order book came in oversubscribed roughly 870 times. The deal was a triumph before he opened his mouth, and the moment asked only for grace. Instead he told the regulators sitting in front of him that they were doing it all wrong. China’s banks ran like pawn shops, he said. The country carried no systemic financial risk because it had no functioning financial system to speak of. Innovation was dying under small men in love with their own paperwork.

Nine days later there was no offering. On the second of November the authorities summoned Ma to what they delicately called a supervisory interview, a joint sitting with the central bank and three other regulators. The next afternoon, with the stock 36 hours from trading, the Shanghai exchange suspended the listing, citing a sudden and unspecified change in the regulatory weather. Hong Kong followed within hours. The Wall Street Journal later reported that the order to kill the deal had come from Xi Jinping himself. Ma had been the nearest thing China had to a folk hero of private enterprise. He more or less vanished. Over the next year the campaign against the platform companies erased well over a trillion dollars of their combined value. Didi, the ride-hailing company, had pushed ahead with a New York listing against the regulators’ plain wishes; it was hounded into delisting within months.

None of this taught Beijing to put the hammer down. The property developers and the tutoring companies would find that out within the year. China’s version of Kim Kardashian, later still. But the hammer, for everything it could flatten, could never do one thing: it could not sit inside a company and stay there. A crackdown lands and then lifts; it does not hold a standing veto over what a platform shows tomorrow morning, or where it raises its next round of money. For that the state needed an instrument it could leave in place, quiet and permanent, reaching only the decisions it cared about and none of the rest. It needed a scalpel to go with the hammer.

The crackdown ended the thing it aimed at. It also did something the planners had not put a price on. It taught private capital that no fortune in China was ever entirely private, that a regulator’s mood could erase a decade of work between a Friday and a Monday. Money does not forget a lesson like that. The campaign sparked what one account later called a yearslong chill across Chinese technology, and the founders who could leave began to look for the door. Keeping a hand on the companies that mattered, without staging another public execution, was the problem Beijing spent the next several years trying to solve (with mixed results).

But the scalpel was already lying on the table. In 2016 the broadcast regulator had called the heads of the big streaming services into a closed room and told them to receive a state stake of one percent or more, a director, and a right to review their content. The next year the Party’s central office and the State Council issued formal guidance piloting the special management share across online news, publishing, and video. By 2021 the cyberspace regulator’s investment fund was taking its quiet one-percent positions across all the platforms that mattered. At ByteDance, three state entities ended up holding the seat at once: the cyberspace fund, a media group run out of the Party’s propaganda department, and the Beijing city government’s investment arm. No headlines marked any of it. A shell company appeared on a filing. A director took a chair. The state let itself in near the head of the table, close enough to decide who edited the news.

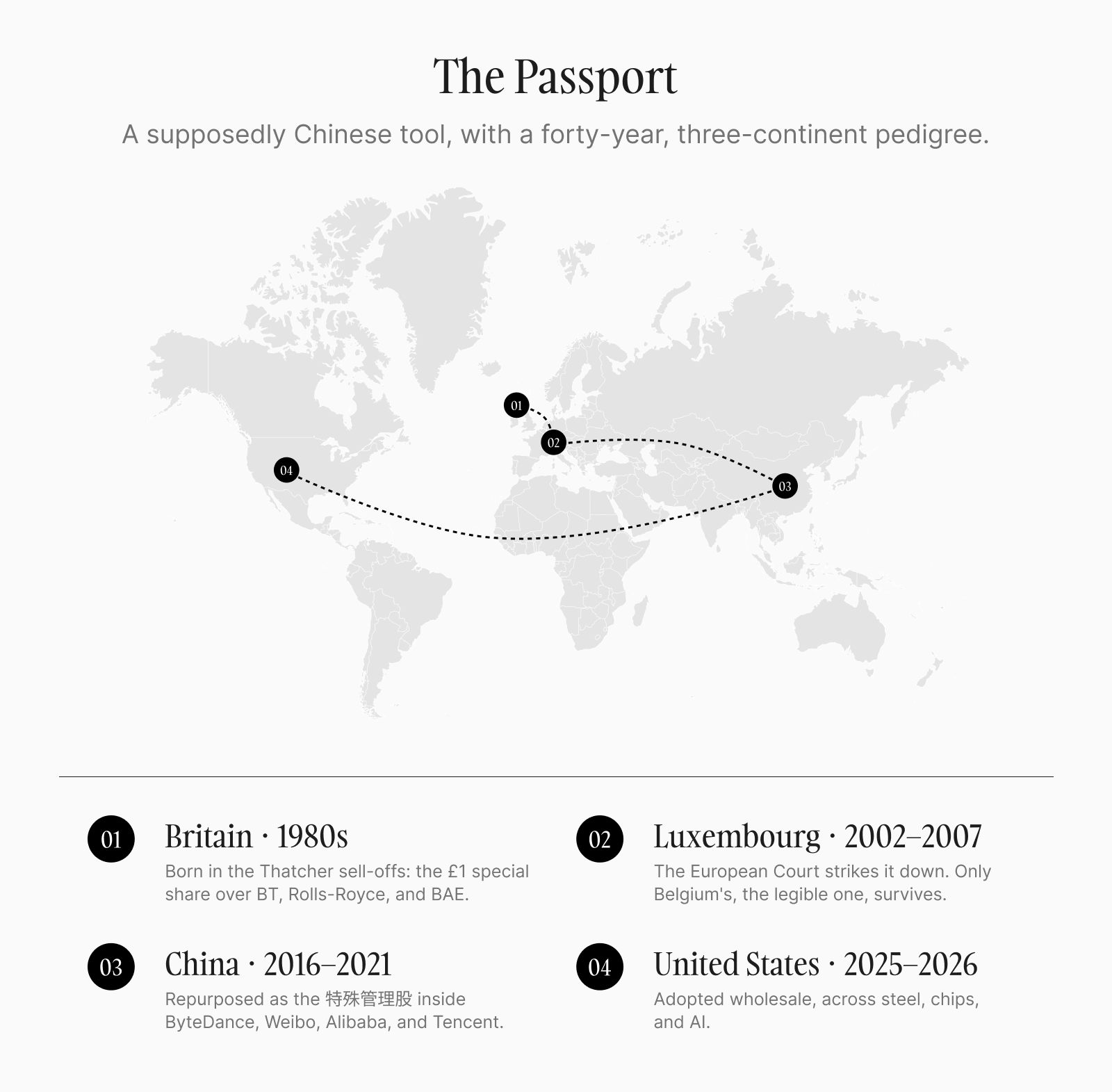

The instrument was not even Beijing’s invention. The special management share was minted in Margaret Thatcher’s Britain, in the privatization sales of the 1980s, to solve an open-market problem: how to hand a state asset to private buyers and keep one hand on the wheel. The government sold the companies and kept, in the ones it cared about, a single special share worth a face value of one pound. It paid no dividend and carried almost no ownership. What it carried was a veto, over a foreign takeover, say, or the sale of a firm that built weapons. Britain still holds golden shares in BAE Systems and Rolls-Royce, the firms that make its warships and the reactors inside its submarines. The logic was plain from the first day. Sell the company; keep the veto. One pound was always enough, because the power in the share had never been tied to the money behind it.

Then Europe spent 20 years stress-testing it. The European Commission decided a government veto hidden inside a privatized company scared off investors from other member states, and it hauled one government after another to the European Court of Justice. The Court struck down the golden shares of France and Portugal, then Spain’s, then the German law that had let the state block a takeover of Volkswagen. One share survived the cull. It was Belgium’s, held over the companies that moved the country’s gas and oil, and it survived for one reason: its powers rested on “precise criteria which are known in advance,” written down, open to challenge before a judge. France’s and Portugal’s were a minister’s prerogative, exercised behind a closed door, and that was the thing the judges would not allow. The version of state control European law could live with was the one you could see.

By the time Washington reached for it, the tool had been tested to destruction on three continents, and the test had returned one clear result: the only state control a free society proved able to tolerate was the kind it could see. The United States was about to run the test again, live, at scale, and largely in public.

The settled wisdom held that it would never reach Washington at all. Almost every other country, rich or poor, keeps a national airline the state owns or stands behind (Singapore Airlines, Emirates), a flag in the sky and a guaranteed line to the rest of the world. The United States never built one, and never thought it should. Its self-image ran on the opposite premise: the government did not own the means of production, did not take seats on corporate boards, and, outside of wartime, did not hold a veto over what a private company sold or where it built a factory. Then, in a single year, it did all three, in the open.

The intent was on paper by the second month of the year. On the third of February, 2025, the President signed an executive order directing the Treasury and Commerce secretaries to draw up a plan for a United States sovereign wealth fund. The aim was to do for the federal balance sheet what Norway does with its oil, to “monetize the asset side of the U.S. balance sheet,” in the Treasury secretary’s phrase. Howard Lutnick, the commerce secretary, a blunt former Wall Street trader who would turn up again and again in the year’s deals, mused that the fund might one day take a profit-earning stake in vaccine makers. The President floated it as the place to park a future American stake in TikTok, the very company whose Chinese parent had taught (or reminded, rather) everyone what a special management share was. The fund has yet to appear. The appetite behind it has, though, over and over.

In June, the government cleared the Japanese conglomerate Nippon Steel to take over U.S. Steel, a deal the previous administration had blocked outright, on one condition: it would receive a golden share, the first the federal government had ever held. The device let an American icon pass to a foreign owner without anyone having to say so plainly. The buyer got the steelmaker. The government kept the veto. And what a veto! It covered closing plants, moving production abroad, reducing Nippon’s promised investment, shifting the headquarters out of Pittsburgh, and even changing the company’s name. It allowed the President to personally appoint one of the three independent directors and block the other two. Every line of that control was written down, in a deal anyone could read. When U.S. Steel moved to idle its works in Granite City, Illinois, and let 800 workers go, the Commerce Department reached for the share and reversed the call. “We have a golden share, which I control,” the President told reporters, pleased. The share has no expiration date. When this administration leaves, it passes intact to the Treasury and Commerce departments, to whoever holds those offices next.

The Intel deal arrived two months later.

Lip-Bu Tan was an unlikely man to find at the center of a national-security drama. He was born in 1959 in Muar, a port town in what was then the Federation of Malaya, into an ethnic Chinese family. He studied physics in Singapore, then crossed to the United States in the 1970s for a doctorate in nuclear engineering at MIT. The meltdown at Three Mile Island soured him on the field, by his own telling, and he dropped out and drifted to Silicon Valley. In 1987, he started a venture firm, Walden International, with 3 million dollars put up by family friends. Over the next 30-odd years he built it into a machine running more than 5 billion dollars and holding stakes in some 600 companies, more than 100 of them in China. One early bet, in 2001, was a seed check to a young foundry called Semiconductor Manufacturing International Corporation, now the largest chipmaker in China; he sat on its board for the better part of two decades. Another was Sina, which went on to create Weibo, which would in time sell its own special management share to the state. In March of 2025, after the board pushed out his predecessor, Tan took the top job at Intel. The company was an American monument in steep decline, its stock down by more than half over the prior year, 15,000 jobs already cut. “Intel is where good reputations go to die,” a veteran Valley executive and friend of Tan’s told the Irish Times, by way of congratulations.

At 4:39 in the morning, Pacific time, on the seventh of August, with Tan presumably asleep in California, the president posted that Intel’s chief executive was “highly CONFLICTED and must resign, immediately.” The trigger was a letter from Senator Tom Cotton, the Arkansas Republican, to Intel’s chairman. It flagged Tan’s tangle of investments in Chinese chip firms, some reportedly tied to the People’s Liberation Army, and noted that Tan had run the design-software company Cadence during a stretch when it sold technology to a Chinese military university, an episode Cadence had recently pleaded guilty to. The two men had never met. The heads of Nvidia and AMD and OpenAI and Google had all made their pilgrimages to the White House. The head of America’s oldest chipmaker had stayed in Santa Clara, and had not given to a presidential campaign in over two decades. He had simply lacked the antenna, one analyst said, to see it coming. Intel’s stock slid on the post. The company put out a stiff line about its commitment to American security.

Four days later the weather reversed. The President received Tan in the Oval Office, flanked by Lutnick and the Treasury secretary, and came out calling the man’s career an “amazing story.” Eleven days after that, on the 22nd of August, the government took a 9.9 percent stake in Intel, buying 433.3 million shares at 20.47 dollars apiece. The whole thing was paid for by converting chip-factory grants Intel had been promised but not yet handed. A warrant let the government buy another five percent if Intel ever lost control of its foundry business. All of it sat in a public filing, the exact share count and the exact price. Fifteen days. In that span, the man the president had demanded resign over his closeness to China became a partner in whose company the United States government was now the largest single shareholder. The accusation had become the acquisition. The president boasted that the shares had cost the taxpayer nothing, an arithmetic that worked only if the grants he had threatened to claw back were counted as money that never existed.

The Nvidia arrangement, that same August, skipped the equity and went straight for the till.

Jensen Huang, Nvidia’s founder, is a showman in a black leather jacket who had spent the better part of a year courting an administration he had been slow to embrace. He was the one major technology chief absent from the inauguration. The courtship began, by his own account, with a cold call from Lutnick, who introduced himself with a formality Huang later found funny enough to repeat on a podcast, and an invitation to come to Florida and sing for his supper. In the spring Huang paid a million dollars a head to dine at Mar-a-Lago, and spent the evening over gold-rimmed plates pressing the President not to choke off his sales to China, a market then worth tens of billions to one of the most valuable companies on earth. He does not take a setback gracefully. Later pressed on the China question, he nearly lost his composure, snapping that he was not someone who had woken up a loser.

What he got was a release on a leash. The administration let Nvidia and AMD resume selling a China-specific chip, the H20, that it had banned in the spring, in exchange for 15 percent of the revenue from those sales, paid to the Treasury, as the price of an export license. Export licenses do not normally carry a fee. The President, who had taken to calling the chip old and obsolete, opened at 20 percent and let Huang talk him down to 15. “I’m giving you a release,” he said. Deborah Elms, a trade-policy analyst at the Hinrich Foundation, named the obvious objection. “You either have a national security problem or you don’t,” she said. A 15 percent cut does not make the danger disappear. It gives the government a stake in the thing it had called dangerous. That is a different posture entirely.

A month earlier the Pentagon had taken a stake of roughly 15 percent in MP Materials, the country’s main rare-earth miner, and become its largest shareholder. The deal set a floor price of 110 dollars a kilogram for the two rare-earth oxides the company sells, close to double the going rate. When the market ran low, the government would pay the gap each quarter. When it ran high, the government would take 30 percent of the upside. It is, almost line for line, the guaranteed-price-and-state-stake structure China had spent two decades perfecting. Until 2022, MP had sold nearly all of its raw output to Shenghe, a Chinese rare-earth company that remains one of its largest shareholders. The American escape from dependence on China was financed by copying China’s method into a company whose biggest customer had been Chinese. This is the case hardest to argue with. A rare-earth supply chain is a chokepoint, and China spent two decades buying up the world’s. When a rival holds the chokepoint and has already shown it will squeeze, keeping both hands off your own scale just leaves you holding nothing. The market that was supposed to allocate the metal had been bent years before, by the other side.

By autumn the habit had reached the ground itself. In October the Energy Department took a five percent stake in Lithium Americas, plus another five percent of the Nevada mine it is digging, for softening the terms of a federal loan. A week later the Defense Department took a 10 percent stake in Trilogy Metals, which wants to pull copper and cobalt out of a remote corner of northwestern Alaska; in exchange the administration agreed to approve a 200-mile access road through wilderness that had been rejected, on environmental grounds, before. None of these was a rescue. That is what made them new. The government had reached for corporate equity before, in the wreckage of 2008, when the Treasury took preferred stock in the banks and the carmakers and sold it back the moment the patient could stand. This ran the other way. The government was buying into, as one researcher in the field put it, “an industry that has not yet launched,” taking positions in things not yet built.

I have argued before that power does not vanish when a new system starts to matter; it rebinds onto it. The state did not nationalize steel or silicon or lithium or rare earth. It left the ownership formally untouched and fastened a fresh hold onto each one anyway: a director here, a cut of the revenue there, a price floor and a guaranteed buyer somewhere else, a warrant that trips if a company stops behaving. The instrument that was supposed to belong to the other side described Washington’s year with uncomfortable precision. And one feature ran through all of it. Every stake had a price, every veto a filing, every trigger spelled out in advance. The government had let itself into a dozen boardrooms, and you could trace, deal by deal, exactly how it got into each one.

None of this was drift. Each move was a choice, and the choice had a target. Washington had watched a state-directed rival outbuild it in steel, in solar, and in the metals that go into both, and decided that a country which keeps both hands off the wheel cannot stay in a race against one that does not. The conclusion may even be right. The trouble is that the method is going badly for the country that wrote it.

China’s strongest decades were its least directed ones, the long stretch after 1978 when the state mostly stepped back and let private firms and foreign capital pull the better part of a billion people out of poverty. The turn back toward control has not paid the way the turn away from it did. Beijing has spent years trying to be strong in everything at once, subsidizing every strategic sector, leaning on its own firms, and squeezing the household spending that a normal economy runs on, in an attempt to force into being a kind of economy that has never existed: a manufacturing superpower that never has to sell very much to its own people. The bill for that arrives slowly, in weak demand and soft confidence and capital that would rather be somewhere else. The crackdown that handed Beijing its quiet instrument was one line on that bill. The country that wrote the method is the one now paying for it.

On the 18th of June, 2026, Senator Bernie Sanders introduced the American AI Sovereign Wealth Fund Act. It would levy a one-time 50 percent tax, payable in stock, on artificial-intelligence companies with more than 200 million dollars in sales. The shares would drop into a sovereign wealth fund. The votes that came with them would go to an independent commission empowered to block company decisions it judged harmful and push the ones it favored. The dividends would go to American households, on the model of the checks Alaska cuts its residents from its oil fund. To the populist left, this was the public taking back what the public’s data had built. The same month, from the far end of the spectrum, the president told reporters he would soon sit down with the AI companies about federal stakes, sketching an outcome in which “the American public essentially becomes a partner.” A democratic socialist and a Republican President, in the same month, reached for the identical instrument: voting shares and a seat on the board, used to block. Each was convinced he was rescuing the country from the other one’s idea.

The two boldest moves either government made all year landed on the same industry, six weeks apart, and neither one broke a law. Both reached into ordinary, legal, voluntary activity and simply stopped it. The people who watch this closely are still arguing about what they saw.

Start with Beijing, in the spring. In December of 2025, Meta had agreed to buy an AI startup called Manus for more than 2 billion dollars, the clean exit that founders across Chinese tech had been waiting for, proof that you could build a company in China and cash out to an American giant. Manus had taken great pains to be acquirable. Built in Wuhan in 2022, it had gone viral in March of 2025 on a demo of an AI agent that carried out long tasks on its own, and by the following summer it had moved its headquarters to Singapore, laid off most of its China staff, cleared its Chinese social accounts, and blocked mainland IP addresses—the full routine a Chinese company performs to read as a global one. On paper, it was Singaporean. But none of it mattered. On the 27th of April, 2026, China’s economic planning agency, through the office that runs its foreign-investment security review, ordered the deal unwound, the first foreign acquisition in artificial intelligence it had ever publicly blocked. The decision reportedly went up to the national-security commission that Xi Jinping chairs. Officials reviewing it described the sale, in the reporting that followed, as an attempt to hollow out the country’s technology base. The thing Beijing was protecting sat underneath the letterhead: the engineering, the training data, and the people—all built on the mainland, none of which it would let walk out the door under another flag.

Washington’s version came six weeks later, and it reached … somehow further.

Dario Amodei makes an unlikely insurgent. He is a physicist, soft-spoken and a little owlish, who led the teams behind GPT-2 and GPT-3 at OpenAI. In December of 2020 he walked out, with his sister Daniela and a handful of colleagues, over what they took to be the organization’s (you would not call it a “company” back then) cavalier attitude toward safety. The lab they built in response, Anthropic, made the Claude models. Amodei spent the next several years in a posture almost nobody else in the industry could hold for long. He wrote a 15,000-word essay imagining that powerful AI might cure most disease and double the human lifespan. In the same breath, and the same calm register, he warned that it might also slip its makers and end very badly. He believed, an admiring reviewer wrote, that the industry was building gods, and that humanity might not survive the building. On a Sunday news program in late 2025 he said that he was “deeply uncomfortable with these decisions being made by a few.”

He meant the company chiefs. He did not yet know how completely the government was about to prove that the “few” people in question were not the ones he had in mind.

Through the early months of 2026, the Defense Department negotiated with Anthropic over the terms on which the military could use Claude. The talks foundered on two points the company would not give up. Anthropic was, by its own account, willing to support nearly any lawful national-security use of its models, with two exceptions: It would not let Claude be turned on the mass surveillance of Americans, nor would it let it run fully autonomous weapons that chose and killed with no human in the loop. The Pentagon wanted access for “all lawful purposes,” and argued that a private contractor had no business telling the government how to use its tools in an emergency. One version the Pentagon floated, according to reporting on the failed talks, would have required access to Americans’ geolocation and financial records, pulled from commercial data brokers.

On the 27th of February, Pete Hegseth, the Secretary of War, a title his department had recently revived from the first half of the 20th century by executive order, announced on social media that he was designating Anthropic a supply-chain risk, a label ordinarily reserved for companies tied to foreign adversaries. The President ordered every federal agency to stop using the company’s technology at once. Anthropic, which said the two exceptions had not blocked a single government mission to that point, sued. In late March a federal judge in San Francisco, Rita Lin, granted an injunction, writing in a blistering opinion that nothing in the law supported the “Orwellian notion“ that an American company could be branded a saboteur of the United States for disagreeing with its government. In April a federal appeals court declined to block the Pentagon in Anthropic’s separate, narrower case, even as Lin’s injunction held. The fight ground on into the summer.

Among the reasons the government gave, in its own court filings, for treating Anthropic as a danger to the nation was this: the company might be able to disable or quietly alter its own model in the middle of a live military operation, if it decided its policies were being crossed. A private firm, in other words, might hold a kill switch over its own technology. The government found that intolerable.

Then, on the afternoon of Friday the 12th of June, at 5:21 Eastern time, the government reached in and threw the switch itself. An export-control directive, citing national-security authority and ostensibly worried about a method of jailbreaking the safeguards on one model, ordered Anthropic to cut off all access to its two most capable systems, Fable 5 and Mythos 5, for every foreign national on earth, including the company’s own foreign-national employees. Anthropic had no way (yet) to sort its users by passport, so it switched both models off for every customer in the world within hours. Weeks earlier the same systems had captivated Wall Street and Washington. By the company’s own account, the letter that turned them off “did not provide specific details“ of the concern behind it.

Set the two side by side. One government stopped a sale; the other switched off a product. One invoked a foreign-investment review; the other invoked export control. Both reached into activity that was legal, voluntary, and already underway, and stopped it cold on the authority of national security, and in neither case had the company on the receiving end broken a law. Meta said the Manus deal “complied fully with applicable law.” Anthropic had been running two products the government itself was using days earlier. No property was seized. No crime was charged. What happened was newer than either, and harder to name: a state deciding that a particular piece of artificial intelligence was too important to be left to the people who owned it, and moving it where the market never would have. Two governments, six weeks apart, at opposite ends of the earth, arrived at the same decision, and reached for it with the same hand.

The honest position starts by conceding the thing the libertarians will not. The state’s grip on the country’s most important companies is now something both parties want (the year just past says so plainly), and against a rival that builds this way, it may simply be the cost of staying in the race.

Where the grip stays narrow, it is defensible. But there is one mistake the United States cannot afford to copy, and it is the one China made. Top-down management has a failure mode that has nothing to do with which sectors a government picks. It frightens the people whose money it needs. Capital that no longer trusts the rules leaves, or hides, or waits; the state moves into the space it vacates; the vacancy frightens the next tranche of capital, and the thing feeds on itself. Confidence is slow to build and quick to break, and breaking it is the surest way to turn a selective intervention into a general retreat. China is several years into learning this. The United States is at the beginning.

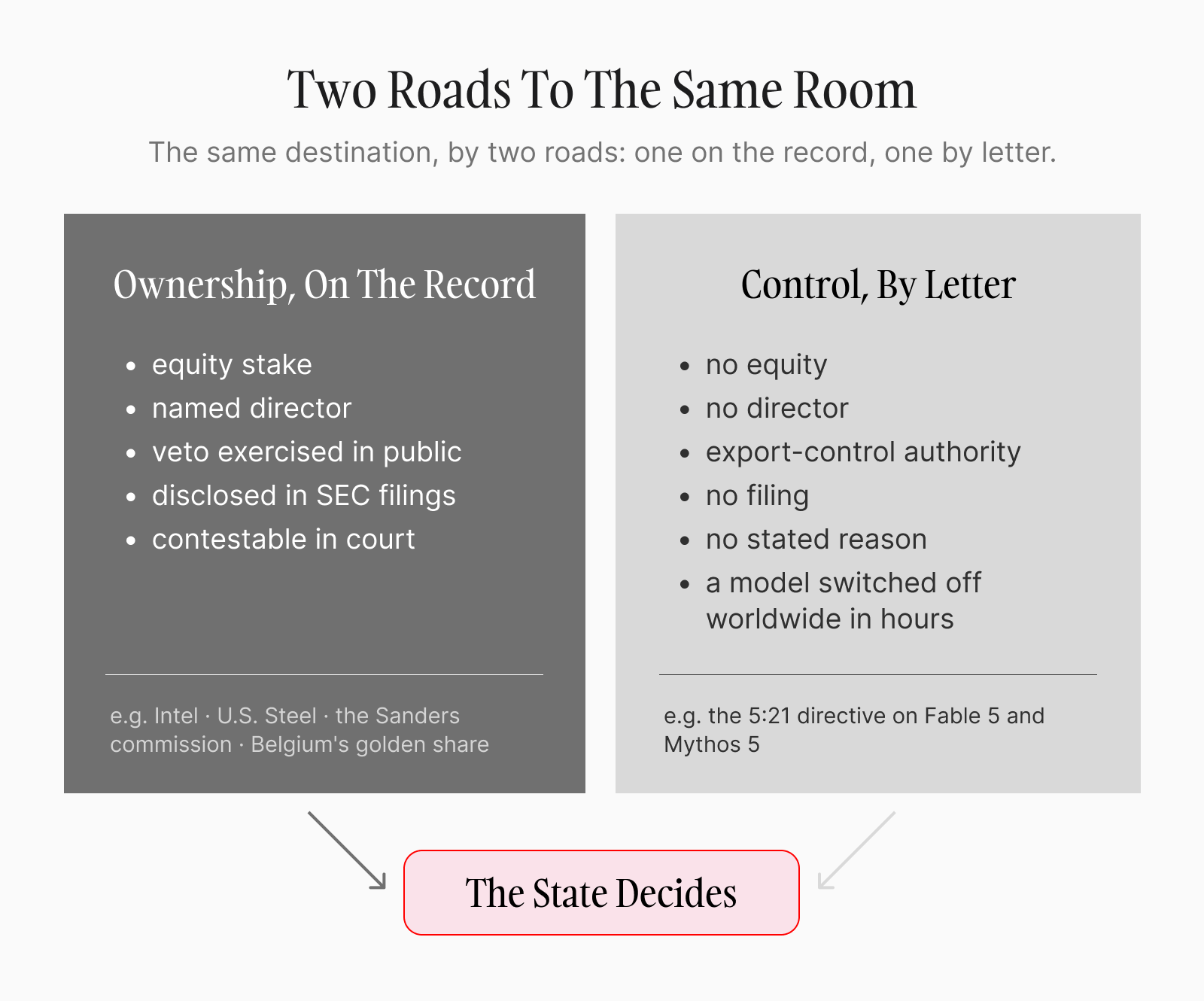

So the form the grip takes decides everything. The equity stake, the thing the libertarian and the hawk both fix their eyes on, is the part that behaves itself. A named director, a disclosed price, a veto exercised somewhere a court can see it: that kind of control is selective by construction, because it has to be argued for in the open and can be fought there. It was the only kind Europe’s judges would let stand. The dangerous instrument is the other one—the one with no filing, no price, and no reason given. China’s review of the Manus deal ran largely in the dark, on grounds it never had to fully spell out. The American letter that switched off two models on a Friday gave no reason at all. Power that leaves no mark on a balance sheet is the more total kind, precisely because there is nothing on the record to point at, and nothing on the record is exactly what teaches capital to be afraid.

The position worth taking is the one almost no one is taking. The argument that the state should be kept out is lost; both parties walked away from it. What is still live is the form. When the state comes in, it should come in an expensive, visible way. Make it buy its share. Sit its director in a chair with a name on it. Put its veto on the record, where the price can be counted and the call fought in open court. Where the intervention is genuinely forced, as it is at a weaponized chokepoint like rare earths, the legible version is the right answer, and a defensible one. The instrument to refuse is the silent letter, because the silent letter is how a country talks itself, one unaccountable decision at a time, into the arbitrariness that empties a room of capital.

None of this is new, which is the unsettling part. Britain built the instrument, and Europe stress-tested it and kept only the version that stayed in the light. China picked it up, reached past it for the blunter tools lying beside it, and is now several years into paying for what those tools did to the confidence of the people it needs most. The United States has spent a single year reaching for the same things, in the same order, under the same logic of necessity, and it has already begun to prefer the quiet version: the letter over the share, the decision no one has to defend.

This has happened before. Twice this spring, in two capitals that agree on almost nothing, a government looked at a piece of the future, decided it was too important to leave in private hands, and took the wheel away from private machinations. The metals and the models are different. The instinct is identical, and so is the long record of what it costs a country when this kind of power stops being selective and stops being seen. The tool can be picked up. It has to be picked up slowly, narrowly, and in daylight, with both eyes on the one mistake that turns an instrument of competition into the thing that hollows a country out from the inside. The warning is not that the state takes a hand. It is what happens when the hand stops leaving fingerprints.